PayIt Blog Government ModernizationHow better reporting improves efficiency in government agenciesMarch 11, 2026Government Modernization2026 government technology trend predictionsDecember 4, 2025Government ModernizationIns and outs of government payment processing admin portalsOctober 9, 2025 TypeCities and countiesDriving AdoptionGovernment ModernizationOutdoorsPeople of PayItResident ExperienceStates and provinces Search

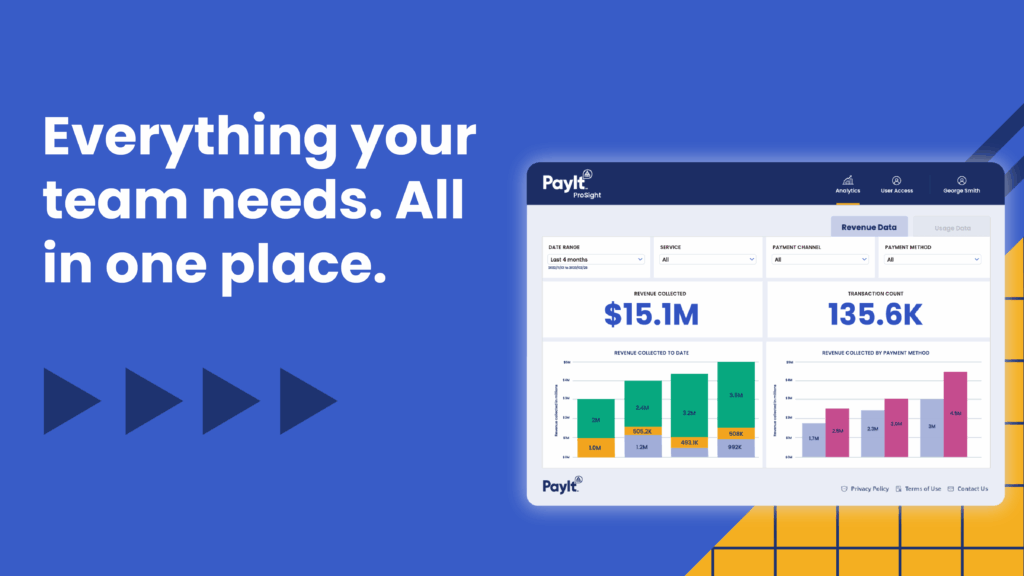

Government ModernizationHow better reporting improves efficiency in government agenciesMarch 11, 2026